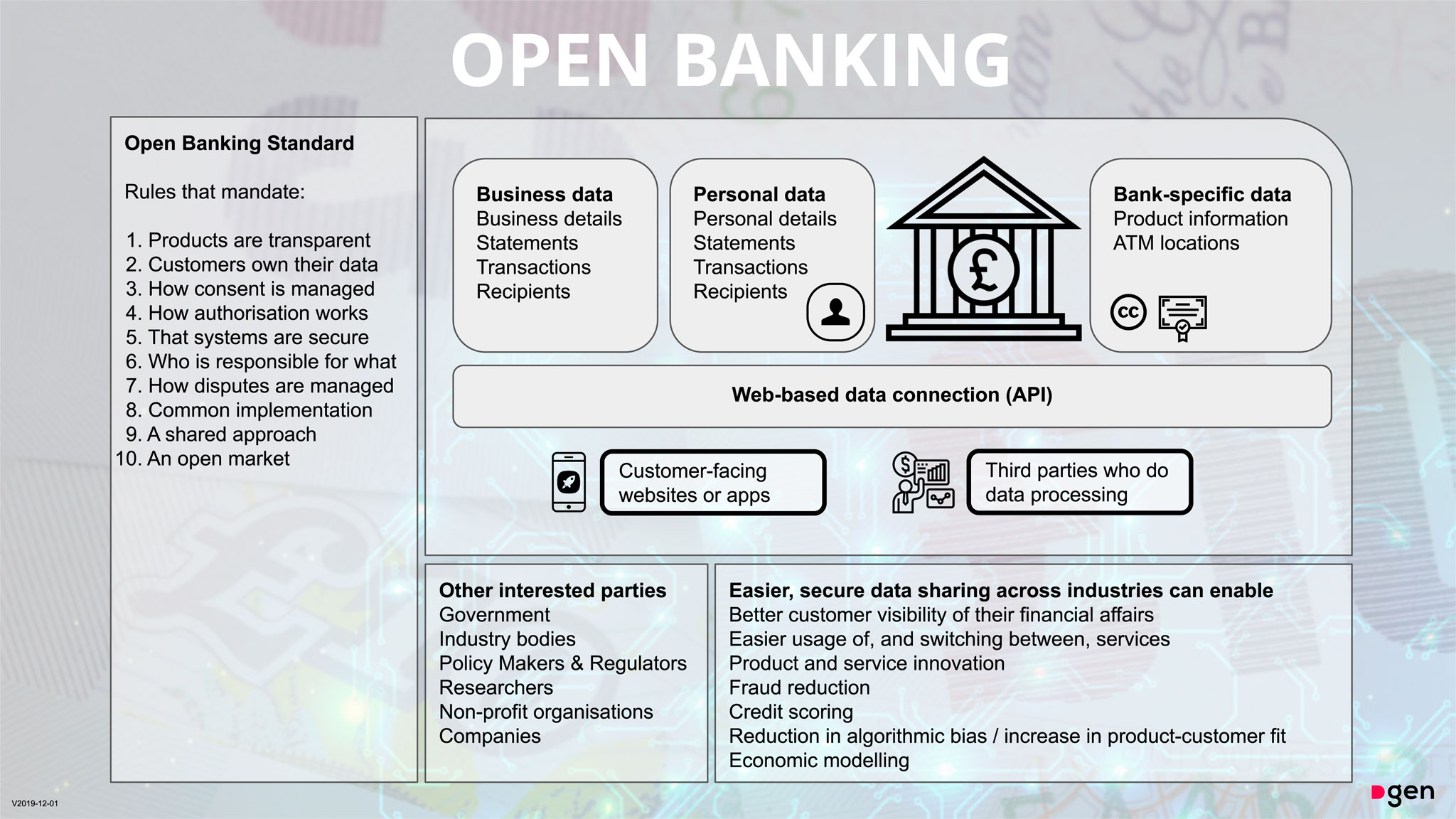

“Open Banking is not a technology. It is a set of standards, principles and practices that lay the foundations for open financial markets in a digital-first economy.

It is part of our financial data infrastructure.”

Open Banking unlocks the open market for banking services in the digital age. It gives customers rights and control over their own banking data – enabling banks to share data in a way that is both compatible with how the web works and protects consumers as they expect from a bank.

Control & consent

Opt in to new services with explicit consent for specific purposes, revocable at any time. Share bank credentials only with your bank – not with third parties.

New products & services

Develop within a clearer, safer ecosystem – with open APIs as a shared, common technical implementation, and open product data for comparison and matching.

Interoperability

Share data compatibly with how the web works, meeting consumer expectations while enabling open APIs for products – savings, credit, loans, mortgages.

A whole-of-market solution

Machine-readable product descriptions enable market-wide comparison and matching – imagine selecting a mortgage by telling the market to make you an offer.

The naming was a conscious design decision by the chairs of the UK’s Open Banking Working Group in 2015. Each word was chosen deliberately:

If the design had not been open, ‘open banking’ would have been owned by the 9 CMA banks. The decisions taken by the Open Banking Working Group in 2015 are the reason that all the work by the OBIE is available under open licence to anyone – including other countries.

Gavin co-chaired the development of the UK Open Banking Standard at the request of HM Treasury, working with the Open Banking Working Group to design the standard that has since catalysed international regulation and an open banking market now valued at over $40 billion.

The Dgen team has since worked with Finance Canada on three reports laying the foundations for open banking internationally, and has conducted a comprehensive review of open banking development across 11 countries. Gavin also co-chaired the UK Smart Data Council and has served as advisor to the FCA on Open Finance, and the Global Open Finance Centre of Excellence.

We have reviewed and worked with countries across:

Interested in open banking, open finance or smart data strategy?